Focus on

THE DIAMOND MARKET

Photo by Mike Benna on Unsplash.com.

CLOSELY FOLLOWED DIAMOND PIPELINE REPORT SAYS

2021 JEWELRY SALES AT RETAIL EQUALED $85.55 BILLION

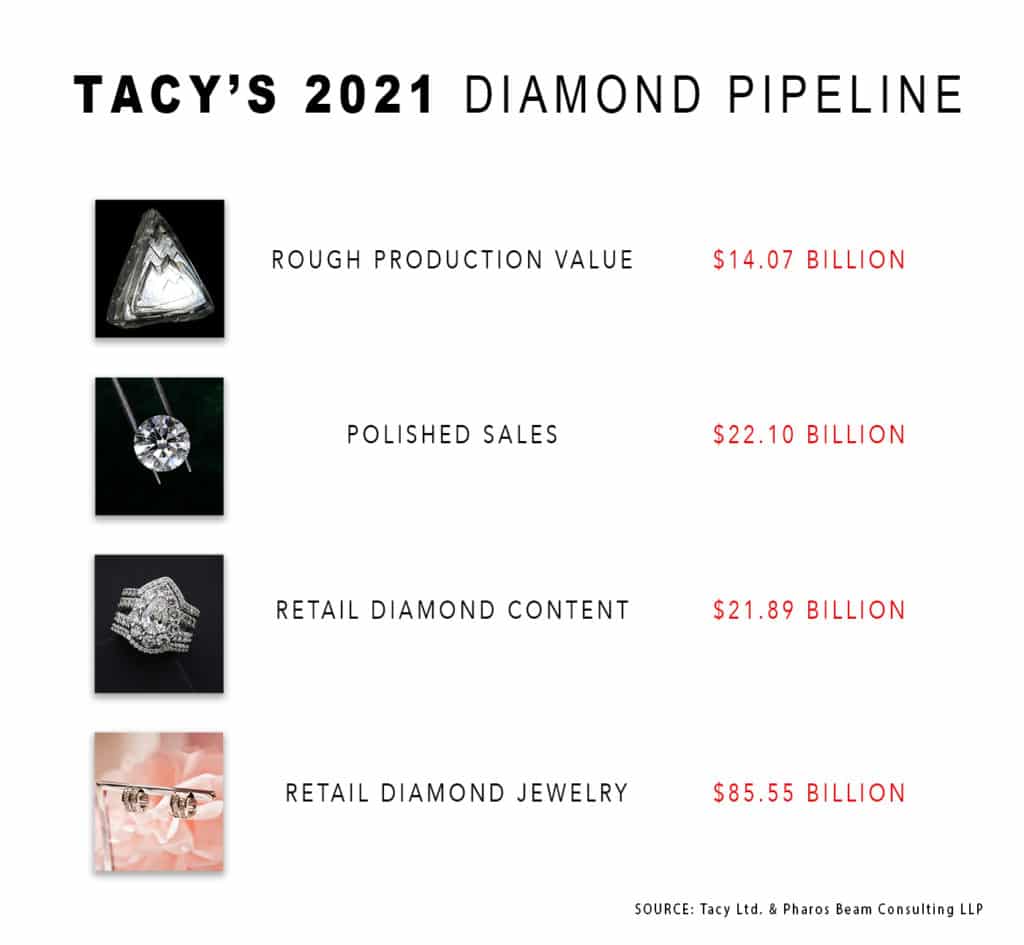

2021 proved to be a spectacular year for the diamond jewelry industry with sales at retail equaling $85.55 billion, and almost 60 percent of them, or $51.23 billion worth, registered in the booming U.S. and Canadian markets, according to the just-published TACY Diamond Pipeline Report prepared Pharos Beam Consulting, and authored by Pranay Narvekar and Chaim Even Zohar.

While the North American market dominated, rising almost by 6 percentage points from a 54 percent market share in 2020, other markets also showed good performance, with China and India both doing well. Overall, the industry showed growth of nearly 32 percent.

And it was not only an improvement in the volume of sales, but in profits as well, the report’s authors stated. While margins were tighter because of a greater proportion of online sales, the surge in demand meant that retailers enjoyed higher pricing power, resulting in less discounting. What also helped was a significant increase in the volume of laboratory-grown diamond sales, where higher profit margins are standard.

Further upstream, sales of loose polished sales increased by about 55 percent compared to 2020, to stand at $22.1 billion. As a result of the higher demand, the midstream was able to reduce overhangs in its inventory. Furthermore, noted the report’s authors, they were able to institute price increases, which averaged between 10 percent and 15 percent over the course of the year

The rise in the volume of sales coincided with the loss in production from the Australia’s Argyle mine, which finally shut down, removing between 2 million and 3 million carats of production of mostly lower-end rough goods. As a result, prices in these quality ranges moved up by about 30 percent to 40 percent, but the shortfall also was managed by the introduction into the pipeline of greater numbers of laboratory-grown diamonds.

Overall, rough producers pumped $15.47 billion worth of merchandise into the pipeline, which was 65 percent more than in 2020, which was a year when disruptions were frequent because of the COVID pandemic.

NORMALIZATION OF LAB GROWN

The 2021 TACY Diamond Pipeline Report, which has been a fixture in the industry for many years, is notable in that it regards laboratory-grown diamond production as a standard addition to the mix of goods entering the pipeline, rather than as a separate category, which to date has been the standard approach.

According to the report, production of rough laboratory-grown diamonds equaled about $1.2 billion in 2021, which is about 8.5 percent of total production. However, in volume terms, because the price of lab-grown diamonds is significantly lower per carat, the actual number of synthetic goods flowing into the pipeline is substantial.

Narvekar and Even-Zohar have taken the relatively controversial position that the normalization of laboratory-grown diamonds in the supply chain in inevitable, not as a separate product category but as part of the regular mix.

“Those who have followed our annual analysis for many years will remember that we have said that eventually the price differentiation between natural and LGD will disappear,” they stated, “and the market will know only one product, called diamonds.”

TIME TO PAY THE BILL

The authors of the TACY report are less confident that the boom of 2021 will continue. The 2021 party seems to be ending, they write, and it may be time to pay the bill.

What they refer to specifically, particularly in terms of the U.S. market, is that the spectacular increase in demand for jewelry, and diamond jewelry in particular, was fueled in part by the series of stimulus packages passed by both the Trump and Biden administrations, so as provide impetus to consumer spending in an economy still feeling the after-effects of COVID. These will not be repeated in 2022, which is already is a year during which an excess of cash in the marketplace has generated a resurgence of inflation.

The financial market scenario now evident was not a surprise, the report’s authors stated, and the diamond industry can be expected to return to its normal state of operation, “besieged by the problems of low growth and insufficient profitability.”

This, they add, does not take into consideration the disruptive effect of the war in Ukraine, and the removal of a major percentage of rough Russian-produced goods because of sanctions. But, they add, “one of the primary strengths of the industry is its resilience and the adaptability of its companies, as it has proven again and again over the decades.”