Focus on

THE DIAMOND MARKET

2020 WAS YEAR OF TWO HALVES, SAYS DE BEERS REPORT,

BUT RECOVERY WAS GENERALLY SWIFT IN 2021

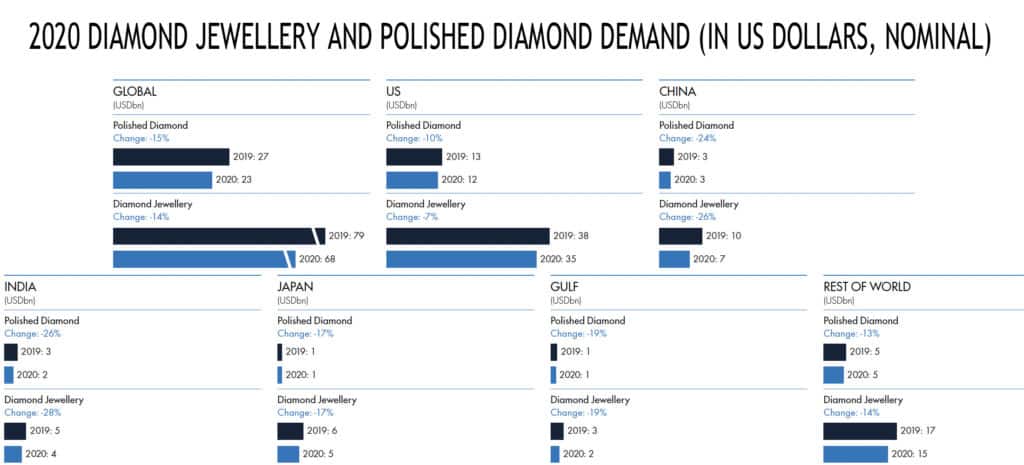

Almost a year later, the final results are in, with conclusive data about COVID-impacted 2020 being provided by De Beers in its recently released Insight Report. According to the document, global demand for diamond jewelry in 2020 declined by an estimated 14 percent year-on-year to $68 billion, mostly as a result of a sharp drop in sales during in the six months of the year, was followed by moderating second six months.

In the words of De Beers, 2020 was a year of two halves for consumer demand for diamonds, with lockdowns and mobility restrictions causing steep declines in consumer demand during the early part of the year, first in China and then in the rest of the world. The second half of the year was a period of gradual improvement.

But 2020 ended on a high note with a positive momentum, despite the global annual decline of in sales value compared with 2019. That recovery picked up pace in the first half of 2021, with an estimated global diamond demand growth of about 40 percent year-on-year, or about 15 percent to 20 percent annualized growth on 2019.

According to De Beers, the outlook for the full year 2021 is positive, with expectations for a strong holiday season, which the company predicts will weather the ongoing risks from the pandemic and the political and economic headwinds in different parts of the world.

AFTER THE RECOVERY, A STOCK SHORTAGE

The midstream of the diamond value chain was impacted by consumer demand shifts as well as supply chain disruptions during 2020, De Beers noted in the Insight 2021 report. Polished diamond stocks started building up in the first half of the year as consumer demand stalled and retailers did not need to restock.

For a short period, the great majority of global cutting and polishing activity came to a complete standstill, largely because of lockdowns that were enforced in India as a result of the spread of COVID-19.

Source: De Beers Insight Report 2021

Manufacturing capacities started building up in the second half of 2020 which resulted in strong demand for rough diamonds, with cutting center rough imports declining only by 1 percent year-on-year during the second half of 2020, while the full year 2020 decline was 28 percent year-on-year.

Better than expected polished demand at the end of 2020 supported polished price recovery and growth, De Beers stated in its report.

During the first half of 2021, a shortage of supply was experienced, as a result of improving consumer demand for diamonds running ahead of stock levels, which had been reduced because of factory closures in India during the second wave of COVID-19 infections.

The resulting polished diamond shortages combined with growing consumer demand supported polished price growth, the De Beers report said.

Source: De Beers Insight Report 2021

DESTOCKING SURPLUS ROUGH SUPPLY

Like the midstream and the retail markets, rough diamond production and sales were disrupted in the early part of 2020, because of the impact of COVID-19 on operations.

Rough diamond sales to cutting centers declined by an estimated 49 per cent year-on-year during the first six months of 2020, the De Beers report stated.

The reduction in rough diamond availabilities limited the impact on rough diamond prices, the report said. During the second half of last year, supply to cutting centers gradually recovered and was only approximately 4 percent below 2019 levels.

The unusual state of affairs enabled rough diamond producers to destock surplus inventory that had built up earlier in the year.

For the full year 2020, global rough diamond production decreased by an estimated 18 percent year-on-year in volume, while rough diamond sales to cutting centers decreased by about 26 percent year-on-year in U.S. dollar terms, De Beers reported.

According to the report, the short-term outlook for rough diamond production is driven by the prospect of continued global economic recovery, with operating capacity back to pre-COVID levels for most producers.

However, the report notes, despite the strong recovery in operating capacity, global rough diamond production is not expected to fully return to where it stood before the pandemic, but this is mainly due to the closure of the Argyle mine in Australia and potentially slow recovery in other production.