Blog

Home » Diamonds blog » A TIME OF RECKONING FOR THE LAB-GROWN DIAMOND INDUSTRY

Focus on

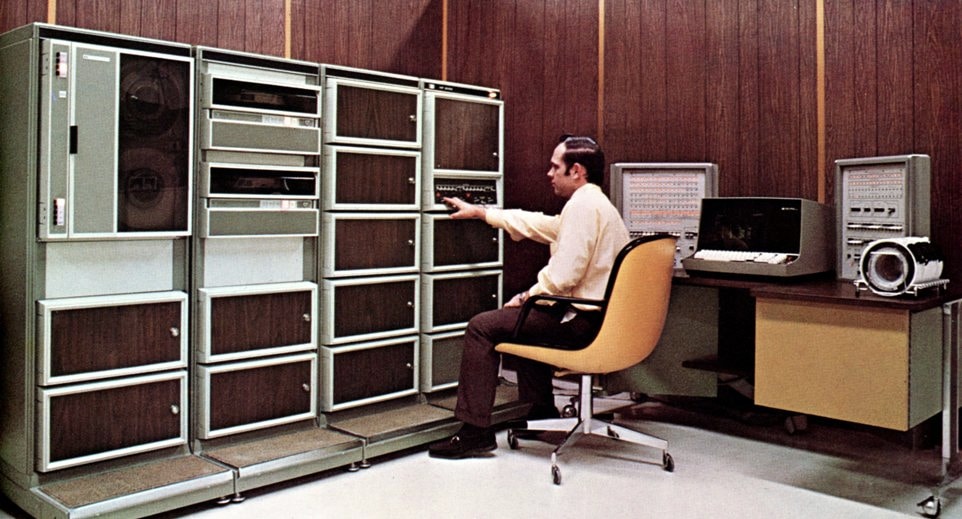

Hewlett-Packard’s HP 3000 series holds a proud place in history. A family of 16-bit and 32-bit minicomputers, it was a system that was considered to a forerunner of the PC, featuring hardware and an operating system that, before it was released in 1972, had been limited to mainframes. At the time it was introduced, such a computer sold for a cool $95,000, which in today’s terms is worth more than half a million dollars.

In 1983, the Apple Corporation released the Lisa. One year before the launch of its more successful Macintosh series, it was the first commercially available personal computer with a graphical user interface. It sold at time for slightly less than $10,000, which in today’s terms would be north of $30,000.

Owning a computer in 1983 was limited to a relatively limited group of generally affluent individuals, a situation that was to change considerably within the space of just a few years. By the 1990s a computer was a standard item in most offices and households, and its price had come down considerably.

Today, if you search the Hewlett-Packard inventory, you will find a range of items on offer that pack a punch that in infinitesimally stronger, faster and easier to operate than the HP 3000. Some are available for less than $400, less than one half of one percent of what the PC’s forerunner cost 50 years ago.

An HP 30000 series computer in 1972. Considered by many to be a forerunner of the PC, it sold for $95,000 at the time.

Hewlett-Packard is still with us because it was able to adjust to the changing market circumstances, but a good number of earlier brands are gone. Firms like Compaq, Wang Laboratories, Sinclair, Palm, Acer, Commodore and Zenith skyrocketed in the early days, but then flamed out and disappeared, because they were not able to adapt like HP did.

A not dissimilar process may be underway in the laboratory-grown diamond industry.

AN EROSION IN REAL VALUE

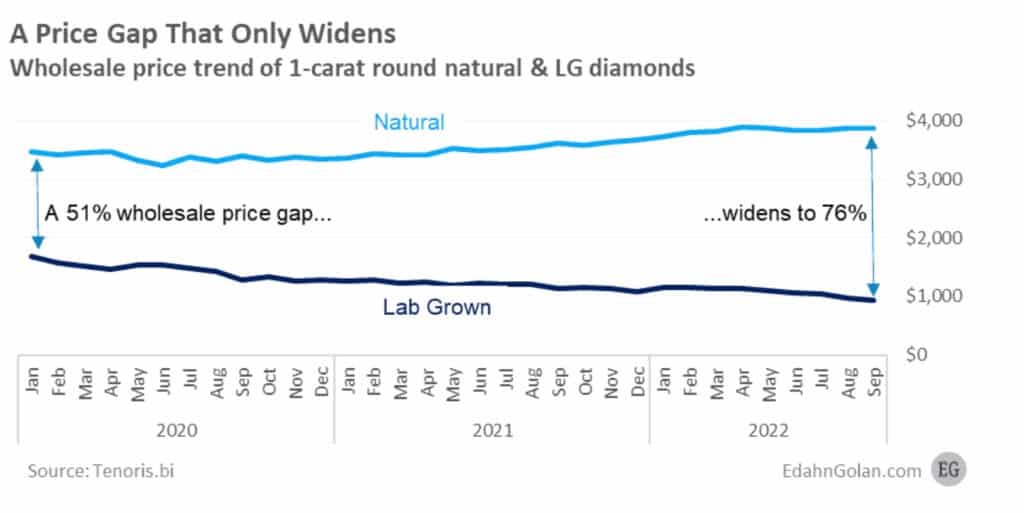

Writing in January, diamond industry analyst Paul Zimnisky noted that as recently as 2016, a one-carat lab-grown diamond sold at a discount of about 10 percent from its natural equivalent. By the end of 2022, the price differential had increased to about 80 percent.

And, said Zimnisky, it’s not only the product that’s coming down in price, but also the equipment that produces it. An off-the-shelf Chemical Vapor Deposition (CVD) machine that sold for much as $300,000 in 2019 can today be purchased in India for under $100,000.

These downward trends, which are likely to continue, should not have surprised anybody. Most economists would have predicted that once mass production techniques were developed and improved, rising consumer demand would increase the rate of production, while reducing the cost per unit. Economies of scale would result in more affordable prices for the consumer.

The problem for the lab-grown diamond industry is that it is being pitched as a luxury product, even as its real value erodes. As long as consumers are prepared to buy into the myth, all is a good and well, but if they begin questioning the real value of what they are being offered, or even worse what they bought several years earlier when the price differential with natural diamonds was smaller, a crisis in consumer confidence may be looming.

MARKETING IS THE PANACEA

The panacea for the lab-grown diamond sector needs to found in how the product is marketed, and that will require it to be sharply differentiated from the natural diamond sector. Lab-grown stones need to develop an identity of their own, which is aspirational but not the same as the identity of traditionally sourced diamonds, whose value proposition is built in because its quantity is finite and mining is an expensive undertaking.

It could be that the model that could be used is similar to that of Swarovski, the producer of jewelry set with crystal glass, which has operated successfully since the Austrian company’s founding in 1895.

There are also lessons to be learned from the fashion industry, where sophisticated branding and marketing have resulted in high-end products being sold for fabulous prices, way above the sum total of the materials from which they are produced.

The common denominator for all such models is substantial investment in marketing, and the question is whether players in the laboratory-grown diamond sector have the ability to do so, individually or collectively through generic marketing.

This is not a rhetoric question. Laboratory-grown diamonds had a tremendous liftoff, during which they gained real market recognition and captured the consumer’s attention and imagination. Furthermore, some real big hitters have invested in their success. These include established brands like Breitling, Swarovski and Pandora.

But more clearly needs to done, and the position of lab-grown diamonds as a luxury product will largely depend how the industry acts in this moment of reckoning.