Home » Diamonds blog » AND THE WINNER OF THE 2019 DIAMOND STAKES…THE CONSUMER

Focus on

THE DIAMOND OUTLOOK

AND THE WINNER OF THE 2019 DIAMOND STAKES…THE CONSUMER

Consumers will emerge clear winners in the current tussle between producers of natural and synthetic diamonds underway in the diamond sector, according to a just-released report, entitled “Diamond Sector Outlook – Entering a Growth and Disruption Phase,” produced by ABN AMRO, the Dutch banking conglomerate that is the diamond and jewelry sector’s largest financier.

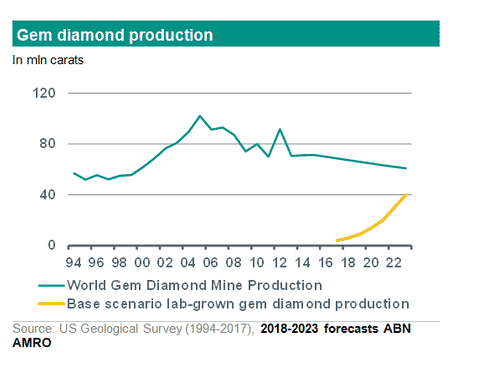

According to the report, which was authored by Georgette Boele, ABN AMRO’s coordinator of FX and Precious Metals Strategy, lab-grown diamonds provide consumers larger and better-quality stones at more affordable prices, as well as a more accessible range of colors.

However, she added, consumers will also have to realize that lab-grown diamonds do not hold investment value.

ROUGH AND POLISHED PRICES THAT ARE MORE IN SYNC

In the report, Ms. Boele forecast lower rough and polished prices for a number of reasons “Natural diamond buyers will scale back their natural diamond purchases because they will probably like to bring down their current inventory and keep it smaller,” she wrote. “With the uncertainty about consumer natural diamond demand and uncertainty over how stable the value of natural diamonds is, buyers are likely to be more cautious.”

But the wide-scale entry of synthetic diamonds into the market may have positive effects on the price structure of natural diamonds, Ms. Boele suggested. This is because of the decreasing influence of miners, who for years have precipitated situations in which the price of rough goods rises at a faster rate than the price of polished materials, resulting in ever-shrinking profit margins in the industry. However, now with more alternatives available to wholesalers and retailers, rough and polished natural diamond prices are more likely to move in sync.

The price of lab-grown diamonds are expected to come under the most pressure, Ms. Boele wrote. “Higher lab-grown diamond production and better technology will drive lab-grown prices lower.”

NEW STRATEGIES FOR NATURAL AND SYNTHETIC PRODUCERS

The general uncertainty about how the market will emerge from this new phase in its history is forcing the different players to adopt new strategies, the ABN AMRO report states. De Beers, for example, announced earlier that it expected output for 2018 to reach 35 to 36 million carats, which would be its highest level since 2008. In 2019 there possibly will be a fall in output, but the output for 2020 and 2021 is expected to surpass the level of 2018. Angola has intimated that it will double production, the report adds.

But others are taking a more cautious approach, such as ALROSA, the Russian diamond producer, which has indicated that it will hold back supply in 2019 to avoid flooding the market.

Miners in general appear concerned about opening new mines, because they are unsure of the rate at which a capital investment will be returned under the new circumstance.

For synthetic diamond producers, the prospect of lower prices requires that their operation become more efficient in order to remain competitive. By finding less expensive and more sustainable sources of energy, they will be able to produce more cheaply, improving their competitiveness, as well as “fight the perception that they may not be as sustainable as perceived,” Ms. Boele wrote.

What also is possible is that natural and synthetic diamond producers join forces, as De Beers showed can be done, when it launched its Lightbox Jewelry line.

“Miners could launch lab-grown diamonds or team up with a lab-grown diamond producer,” Ms. Boele suggested. “We think this will increase the future survival changes of a natural diamond miner.”