Focus on

THE DIAMOND INDUSTRY

BAIN-AWDC: AFTER BRILLIANT RECOVERY FROM COVID CRISIS,

DIAMOND INDUSTRY POISED FOR FURTHER GROWTH

Following a rollercoaster 2020, during which the diamond industry proved its resiliency, a “brilliant recovery” was staged in 2021, with every sector of the industry performing well, noted Bain & Company and the Antwerp World Diamond Center, in the 11th of their annual reports on the diamond industry. The market is expected to remain strong through the first half of 2022, the research paper added.

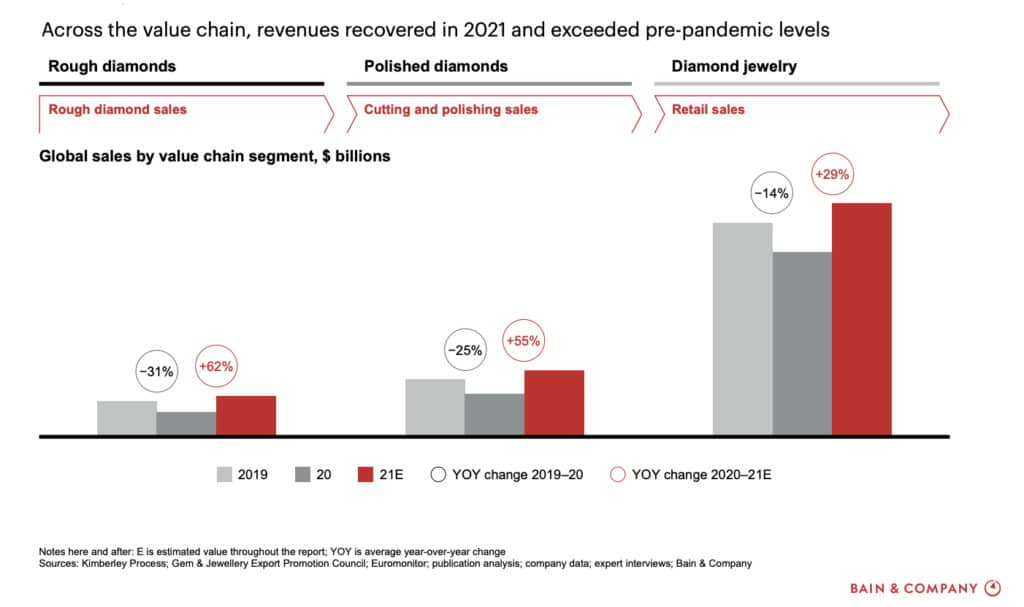

In 2020, as the COVID-19 crisis struck, global diamond jewelry sales fell by 14 percent and rough diamond sales declined by a staggering 31 percent, the report stated. But then, industry revenues rebounded faster than forecast, and in short order exceeded 2019 levels.

In 2021, the report noted, income rose by 62 percent in the diamond mining segment, 55 percent in the cutting and polishing sector, and 29 percent at for diamond jewelry retail. This was 13 percent, 16 percent and 11 percent, respectively, above pre-pandemic levels.

The trend was consistent with previous economic downturns, when the diamond industry recovered with high double-digit growth within 12 to 18 months after a crisis peak, the Bain-AWDC report pointed out.

ROUGH SALES RALLY, BUT INVENTORIES FALL

Rough diamond sales were up by 62 percent in 2021, the Bain-AWDC report noted, with mining companies increasing production volumes and drawing from existing inventories to satisfy strong demand from cutters and polishers.

By the end 2021, mining companies’ inventories reached historically low levels—about 29 million carats, but robust sales, rising prices and cost-cutting programs that were introduced during the in the first half of 2021 saw them enjoying 9 percent to 11 percent improvements on margins on average.

Rough diamond production is expected to be more than 120 million carats in 2022, but it still is unlikely to reach pre-pandemic levels for the next five years. The mining companies remain cognizant that new coronavirus strains could continue threaten production capacity in the short-term, and no major new projects have been announced.

Investments in diamond exploration are still limited, so production growth will likely stay at 1 percent to 2 percent per year during the next half-decade, the report added.

ACTIVITY SURGES IN THE CUTTING CENTERS

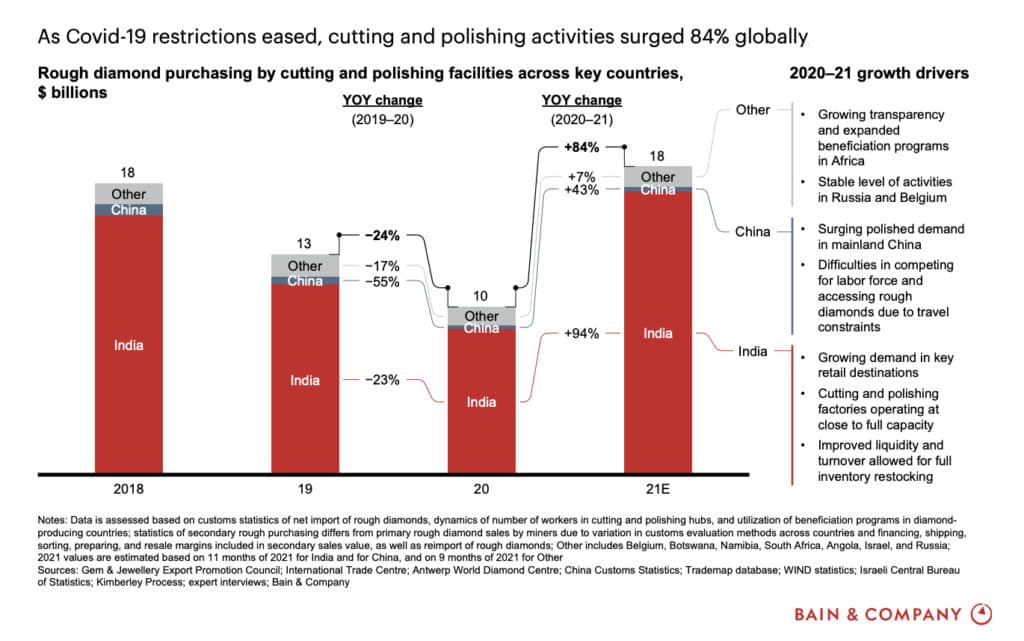

Revenues in the cutting and polishing sector had fallen by 25 percent in 2020, dragged down by disruptions across the value chain, a decline in jewelry sales due to lockdowns, and an average 5 percent fall in diamond prices. But a stronger-than-expected holiday season saw the year end of a positive trajectory, and healthy demand and polished price recovery delivered decade-high margins in 2021.

Demand was global, with increased demand for diamond jewelry in the United States, and an expansion of the diamond footprint in smaller Chinese cities.

Polished diamond sales rose by 55 percent, with the biggest winners in the industry being those who had the foresight and cash to buy rough diamonds at 30 percent to 40 percent discounts between March and September 2020.

In 2021, Indian cutters and polishers increased their net rough purchases by 94 percent, the report noted, to satisfy strong demand from retail. A second wave of COVID-19 lockdowns decreased labor availability in India during the second quarter, but they were short-lived, largely because of vaccinations

In China, the cutting and polishing saw a 43 percent increase in activity, although this was still below pre-pandemic levels. But China’s jewelry market recovered rapidly, driving an increase in imports of rough diamonds.

In 2022 and 2023, the authors of the Bain-AWDC report predicted, midstream performance will be largely influenced by diamond jewelry retail performance, expectations for continued growth in demand and consumer sentiment, and access to a limited supply of rough diamonds.

“Regardless of the market situation, midstream players that have secured access to primary rough supply via partnerships or sightholder agreements and that invest in new technologies and optimize sales operations will benefit the most,” they wrote. “It will be important to watch out for the direction in rough and polished prices. The gap between rough and polished prices will define overall midstream segment profitability, the effect of which we will see in full by mid-2022.”