Focus on

THE DIAMOND MARKET

Photo: Christian Wiediger on Unsplash.com.

CHINESE MARKET MAY FINALLY BE TICKING UP,

BUT IN THE UNITED STATES SIGNS ARE MIXED

While sales in China appear to be spiking upward, indicating that the giant economy is slowly reviving from its COVID-induced slumber, the opposite appears true for the world’s largest jewelry market, the United States.

According to first quarter sales results reported by LVMH, the world’s largest luxury company, sales in China rebounded by more than twice the amount that the analysts forecast, expectations, in the United States demand is showing signs of slippage, particularly among younger, lower-spending shoppers.

Sales by the company, which owns the Louis Vuitton, Dior and Tiffany & Co., came to 21.04 billion euros ($23.10 billion) for the three months to end-March. LVMH said first-quarter sales grew by 14 percent in Asia, excluding Japan, compared with an 8 fall decline in the fourth quarter of last year. It added that said expected China to drive growth in 2023.

U.S. sales were actually up by 8 percent during the quarter, but according to LVMH’s finance chief most of that growth could be attributed to strong sales at its Sephora retail chain of beauty and cosmetic stores.

“For the rest, the business is slowing down a bit,” Jean Jacques Guion was quoted by Reuters, noting softer demand for fashion and jewelry.

NRF STLL REMAINS OPTIMISTIC

The data released by LVMH did not seems at odds with figures provided by the U.S. Department of Commerce, which reported that watch and jewelry sales in the country fell for the fifth consecutive month, by 3 percent in February. Ongoing fears of a recession and financial crisis, were cited.

According to the U.S. Department of Commerce, jewelry sales slipped by 3.4 percent and watch sales by 1.4 percent during February. In January, sales had fallen by a more modest 0.3 percent.

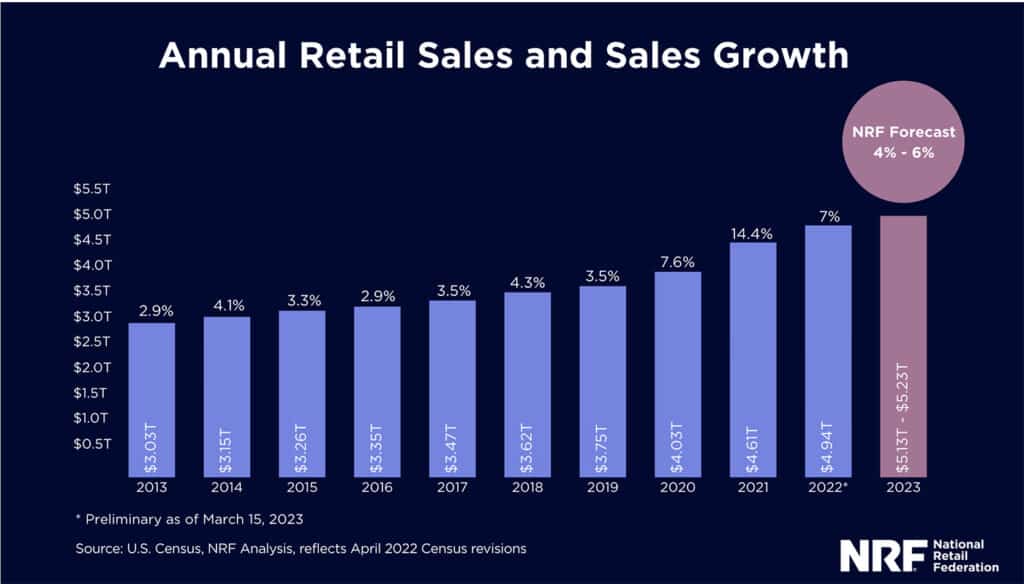

The National Retail Federation remains optimistic, however, anticipating that sales will grow between 4 percent and 6 percent in 2023. In total, NRF projects that U.S. retail sales will reach between $5.13 trillion and $5.23 trillion this year.

“In just the last three years, the retail industry has experienced growth that would normally take almost a decade by pre-pandemic standards,” NRF President and CEO Matthew Shay said. “While we expect growth to moderate in the year ahead, it will remain positive as retail sales stabilize to more historical levels.

The 2023 figure compares with 7 percent annual growth to $4.9 trillion in 2022. The 2023 forecast is above the pre-pandemic, average annual retail sales growth rate of 3.6 percent.

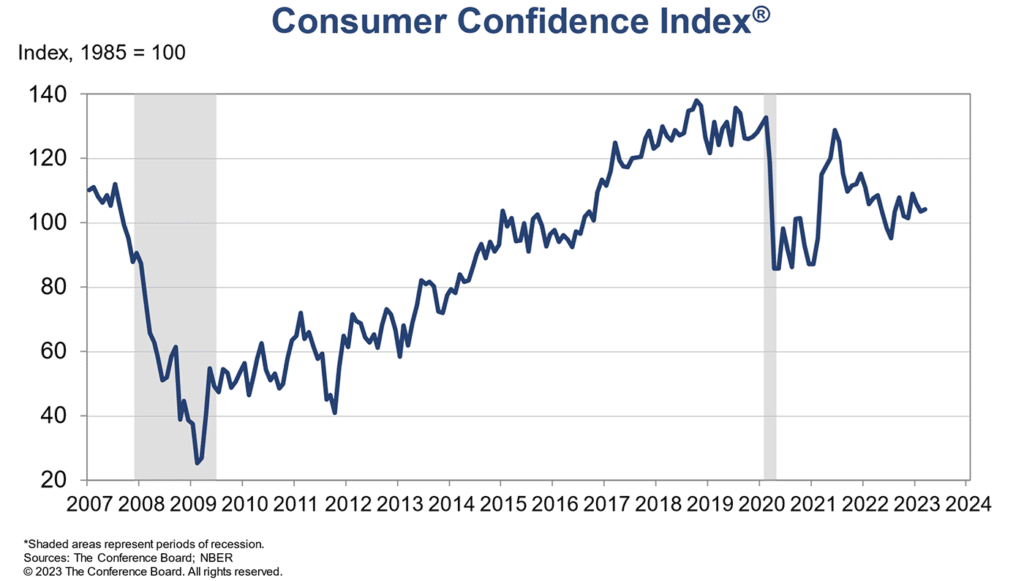

CONSUMER CONFIDENCE RISES SLIGHTLY

More in line with the NRF data, the Conference Board’s index of U.S. consumer confidence increased slightly in March to 104.2 (1985=100), up from 103.4 in February. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—decreased to 151.1 from 153.0 last month. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—ticked up to 73.0 from 70.4 in February.

However, for 12 of the last 13 months—since February 2022—the Expectations Index has been below 80, the level which often signals a recession within the next year.

“Driven by an uptick in expectations, consumer confidence improved somewhat in March, but remains below the average level seen in 2022 . The gain reflects an improved outlook for consumers under 55 years of age and for households earning $50,000 and over,” said Ataman Ozyildirim, Senior Director, Economics at The Conference Board.

“While consumers feel a bit more confident about what’s ahead, they are slightly less optimistic about the current landscape. The share of consumers saying jobs are ‘plentiful’ fell, while the share of those saying jobs are ‘not so plentiful’ rose. The latest results also reveal that their expectations of inflation over the next 12 months remains elevated—at 6.3 percent. “

18.4 percent of American consumers said business conditions were “good,” up slightly from 18.0 percent. However, 19.3 percent said business conditions were “bad,” up from 17.4 percent.