Focus on

the diamond industry

DIAMOND INDUSTRY EMERGING FROM COVID RELATIVELY HEALTHY, SAY BAIN & CO. AND AWDC IN ANNUAL REPORT

While the COVID-19 crisis represented a massive challenge for the diamond industry, as it did for many other sectors, particularly in the luxury product business, on balance its consequences could have been considerably worse, according to the latest annual Diamond Industry Report, just published by Bain & Company and the Antwerp World Diamond Center (AWDC).

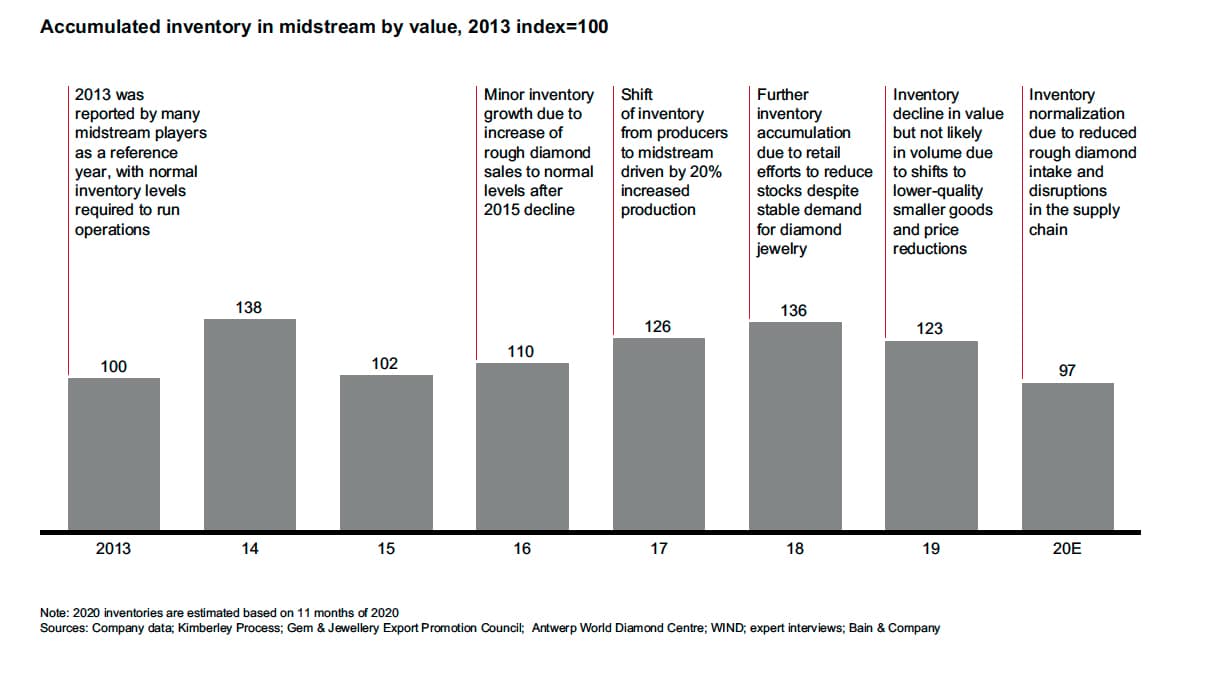

As things are, midstream players cleared existing stockpiles even further and reduced inventories by 22 percent. Demand for polished diamonds increased in the second half of 2020, leading to a polished price recovery and only a 3 percent decrease year over year.

Profitability moved from near break-even in prior years to 3 percent to 5 percent margins, the report noted, with cutters and polishers of high-quality diamonds benefitting the most, since demand for the diamonds they handle was 2020strong during the second half of the year.

A key element in the midstream’s ability to weather the storm was the mining sector, the report said. Major miners both canceled sales in the first half of 2020 and also allowed clients to postpone purchases. Their own inventories of rough diamonds grew to 65 million carats by the end of third quarter, before decreasing to 52 million carats on the strength of the fourth-quarter sales, which still was 17 percent more than where they stood at the end of 2019.

INDUSTRY INDEBTEDNESS FALL DRAMATICALLY

According to the Bain/AWDC report, industry debt levels decreased to $8 billion in 2020, which is about half compared to where they stood at their peak level in 2013. Financing decreased because of lower trading levels and a higher reliance on self financing, the report said.

Outstanding debt in the midstream decreased by 23 percent year over year, and this aligned with generally reduced activity levels in 2020. Financing institutions helped by extended due dates and canceling credit facility fees.

The lack of bank financing had been an issue prior to the start of the COVID crisis, but over the past year new sources of financing became available from specialized funds and peer-to-peer lenders. The alternative financing options are largely geared toward smaller players in the industry, the report stated.

With a significant decrease in rough diamond sales, midstream inventories returneto some of the lowest levels in a decade, the Bain/AWDC report stated.

(*Click to enlarge)

According to the report’s authors, deleveraging is expected to speed up restructuring and consolidation of the midstream in the immediate future, creating long-term benefits across the pipeline.

According to the report’s authors, deleveraging is expected to speed up restructuring and consolidation of the midstream in the immediate future, creating long-term benefits across the pipeline.

BAIN AND AWDC LOOK TO PROMISING FUTURE

Looking forward, the report said that performance in the midstream of the diamond pipeline will depend on how players collectively respond to two factors – downstream demand for polished diamonds after the holiday season, and new sales agreements and rough price policies developed by major miners.

If the rollout of the COVID-19 vaccine is successful, the report said, economic recovery to pre-pandemic levels is expected in 2021–23, with rough diamond production recovering to a “new normal” in the next two to three years and then remaining stable through 2030.

Demand for diamond jewelry is forecast to recover to pre-pandemic levels between 2022 and 2024, the report stated.

Furthermore, if fundamental factors such as GDP and middle and high-net-worth class growth are as strong as projected, as well as sufficient marketing support, then long-term demand will increase at an average annual rate up to 2 percent to 3 percent from 2023 through 2030.

Over the the long term, the global economy is projected to grow at an annual rate of 3 percent, with the United States, China and India leading the growth in diamond jewelry purchasing.

“We expect the U.S. economy and personal disposable income to grow around 2 percent annually,” the report’s authors wrote. “In China, diamond jewelry demand will be driven by 4 percent growth in affluent and high-net-worth individuals and from expanded retail footprints in lower-tier cities. In India, diamond jewelry demand will follow middle-class growth (10 percent annually) and be reinforced by the country’s affinity for jewelry and the expansion of internationally branded retailers.”

Nonetheless, the report does point out several factors that could disrupt the supply-demand balance in the short term or slow down the longer-term global trajectory. This includes the U.S. Congress failing to agree on new stimulus programs, escalating trade wars between the United States and China, European debt or currency crises, India’s increased vulnerability to oil prices and or increased taxation to cope with budget deficits.

Sustained consumer fears about COVID-19 and new restrictions to stop its spread are additional risks that could impede recovery, the report said, and greater competition from alternative luxury goods is another potential threat.