DISRUPTIVE TECHNOLOGY AND NEW GENERATION TRANSFORMING MARKETS

2017 was a successful year for the luxury markets, with resurgent economies in the Europe and China driving growth in the previously U.S.-centric luxury markets. And jewelry was among the leaders of the pack, showing about 10 percent growth when compared to 2016. But it was also a time of unsettling change, partly because of the growing dominance of Millennial and even younger consumers, whose preferences and buying habits are different to the generations that preceded them, and also in part because of the influence of disruptive technologies.

Indeed, change is the one constant that can be expected moving forward, noted Claudia D’Arpizio, a partner and luxury industry expert at Bain & Company, who spoke on January 19 at the VISIO.NEXT summit at the VICENZAORO January jewelry show in Vicenza, Italy, focusing on the future of the jewelry trade during a transformational time for business in general.

Younger buyers are already the main growth engine of the market, D’Arpizio stated, with 85 percent of new sales in 2017 fueled by Millennials, also known as Generation Y, together with their even more youthful counterparts, known as Generation Z. Brands that have managed to tailor their products and marketing messages to best meet these consumers’ specific tastes and behaviors are the ones that have experienced the most significant increases in sales.

But the shifting values of new generations are not new to experienced marketers, who over the years have frequently had to adapt to the way in which they pitch their products. What is new, however, are the innovative and disruptive digital and cyber technologies, which already are transforming the way in which jewelry is distributed and sold.

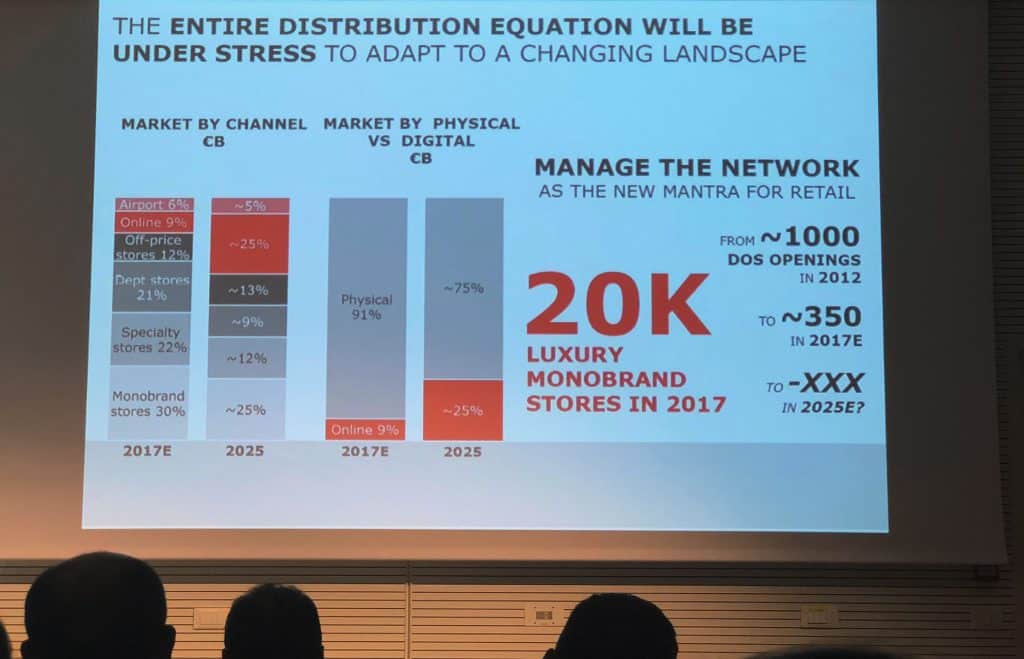

Between 2013 and 2016, online sales of luxury products grew at a compound annual rate of 25 percent, D’Arpizio said, and 24 percent growth can be expected in both 2017 and 2018. About 9 percent of all luxury product sales were made online in 2017, but that will rise to 25 percent within the next eight years, she said. In the jewelry industry, the rise is likely to be less dramatic, growing from about 5 percent at retail in 2016, to between 10 percent and 15 percent by 2025.

Claudia D’Arpizio, a partner and luxury industry expert at Bain & Company, speaking at the VISIO.NEXT summit on January 19, and outlining the massive transformation of the way luxury products, including jewelry, will be bought and sold.

Research by Bain & Co.’s luxury unit indicate that dramatic shift in the channels through which luxury products, including jewelry, will take place over the coming seven years. Significantly, fewer brick and mortar stores will be operating, and their role will change into the place that predominantly the consumer will be able to physically experience the brand and the product.

Jewelry companies that fail to establish an online sales capability will not only be missing out on the fastest growing category in the market, but ultimately may find themselves unable to compete in a business that is becoming “an interdependent and integrated ecosystem,” with both wholesalers and retailers able to reach out to the end-consumer by way of the Internet. To co-exist, these two sectors will need to harness the power provided by the new technology in a mutually beneficial way.

Consumers are being provided with an increasing array of tools to seek out luxury products, and ultimately to buy them at the most attractive price. Jewelers that invest all their efforts in a single channel, such as a brick and mortar store, may find themselves becoming obsolete.

This is not to say that the jewelry store will not remain an important component of the business, D’Arpizio stated, but it will not necessarily be the place where the final sale is made. The store is where the consumer can physically experience the brand or the item of jewelry, but the decision of what to buy, and what price, is increasingly likely to be made online.