Home » Diamonds blog » Luxury Market Shifts as Chinese Buyers Stay Home

Focus on

the luxury markets

MAJOR SHIFT IN WORLD LUXURY MARKET, AS A GROWING NUMBER OF CHINESE BUYERS STAY HOME

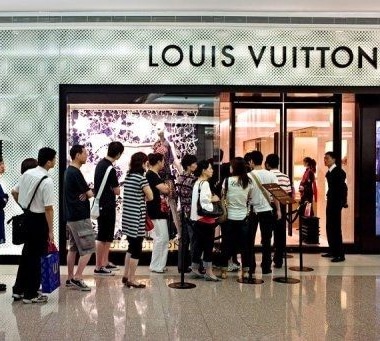

Over the past decade, as growing Chinese affluence translated into a dramatic rise in overseas travel, tourists from the country became the mainstay of the luxury goods business in a wide variety of nations, and particularly so in Europe.

According to a Bain & Co. study, in 2018 about one-third of global spending on luxury goods was credited to Chinese consumers, and the consultancy firm predicted that this would this to rise to 50 percent by 2025.

Before the pandemic, Chinese consumers were propping up many brands almost single-handedly. Bain reported that they were responsible for around 90 percent of personal luxury goods growth in 2019, with their share of global luxury sales rising from 33 percent in 2018 to 35 percent 12 months later. Most of of their buying took place outside of China.

Luxury brands had reacted accordingly, hiring Mandarin-speaking sales staff and accepting Chinese payment methods, as well as connecting with the dominant Chinese marketing and sales platforms, such as WeChat.

But then the coronavirus pandemic struck, first in China, where the country’s government reacted with a lockdown that eventually brough the infection rate under control, but practically paralyzed travel both domestically and abroad.

In 2019 some 150 million Chinese citizens traveled overseas, and they were responsible for some 16 percent of the world’s total international tourist expenditure. That ground to an almost complete halt in 2020.

BEIJING LOOKS TO KEEP CONSUMPTION AT HOME

But the shift to a more domestic focused Chinese consumer market had begun prior to the pandemic, with the central government in Beijing slashing the value-added tax (VAT) rate early in 2019, which was a move that significantly narrowed the price gap between China and elsewhere for many luxury items.

The devaluation of the yuan last summer, which was a move severely criticized by the Trump administration, provided a further incentive for Chinese shoppers to rather shop for big-ticket items at home.

The results of this change became evident in the Spring, when China began reopening its economy after the lockdown with consumers heading back in droves to the retail malls. Foreign brands took note, with the China unit of LVMH Moët Hennessy recording 65 percent growth year-over-year in the second quarter of 2020, while Kering SA recorded a 40 percent increase in revenue in China.

In contrast global revenue at LVMH was down 38 percent and at Kering was 44 percent down.

Before the pandemic, Chinese consumers were responsible for around 90 percent of personal luxury goods growth in 2019. Most of their buying took place outside of China.

In 2019 some 150 million Chinese citizens traveled overseas. That ground to an almost complete halt in 2020.

CHINESE LESS LIKELY TO SHOP AS THEY ONCE DID

In Europe, the effects have been devastating. According to the Altagamma Foundation, which produces the luxury report with Bain & Co., Chinese nationals represented about 50 percent of demand for Swiss watches. In 2020 Swiss watch exports declined by 33 percent year-to-date, which is the sharpest and deepest decline in the last 20 years.

The effect on the European luxury product industry is likely to be prolonged, said Hans Peter, a former CEO of Gübelin, one of the largest Swiss jewelry and hard luxury retailers, speaking to Forbes. “I am quite confident that the Chinese will eventually come back,” he said. “The question is will they continue to shop as they did. It is quite possible that the Chinese government will encourage their citizens to buy luxury products increasingly at home.”

That is a valid question, for such as approach would be in line with the Chinese government’s policy of encouraging the growth of the domestic market, as the economy shifts from being manufacturing dominant to being more consumption dominant.

In the context of the Chinese Communist Party’s Fourth Industrial Revolution, the country’s economy is migrating from an investment-driven model to a consumption and services-driven model.

From 2016 to 2027, Chinese consumption is expected to grow by an average 6 percent annually to nearly $8.2 trillion in 2027. It will be stimulated by the fast-expanding middle class, which will comprise an estimated 65 percent of households just 17 years from now.