Home » Diamonds blog » Diamond Industry Faces Tough 2019, Full Recovery Seen in 2021

Focus on

THE DIAMOND JEWELRY MARTKETS

REPORT SAYS DIAMOND INDUSTRY EXPERIENCED TOUGH 2019, FULL RECOVERY AND GROWTH MOST LIKELY IN 2021

Global diamond jewelry retail sales are forecast to fall by up to 2 percent in U.S. dollar, although when calculated in local currencies will remain stable, noted the ninth annual report on the global diamond industry, prepared by the Antwerp World Diamond Center (AWDC) and Bain & Company.

The slip in sales is being driven by changes in the United States and China, two world’s largest markets, where jewelry sales are expected to decline by 2 percent and 5 percent, the report said, basing its predictions on the results registered during the first three quarter of the year. Consequently, the possibility still remains that remains that the end-of-the-year holiday season may reverse that trend.

In the United States, states the report, the downturn is the result of shrinking consumer confidence, a decline in Chinese tourists, and the 15 percent tariff on Chinese jewelry that went into effect in September. Despite a shift toward local consumption, the diamond jewelry market in Greater China is also expected to decline.

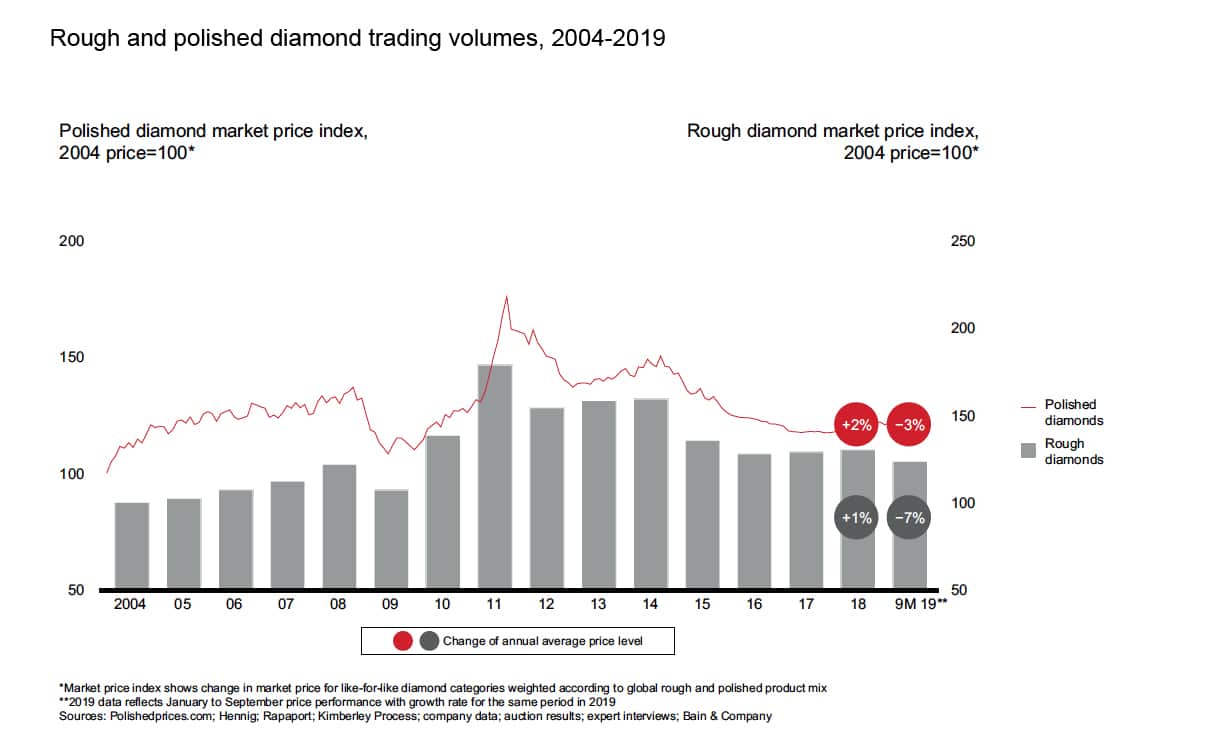

Reduced demand for polished diamonds has led to a 3 percent cut in polished prices and is expected to lead to 10 percent to 15 percent lower revenues for midstream players, the report notes. The slowdown resulted in some of the lowest profit margins experienced in years, as well as high inventory levels, which have been accumulating since 2017.

A LINGERING INVENTORY BACKLOG

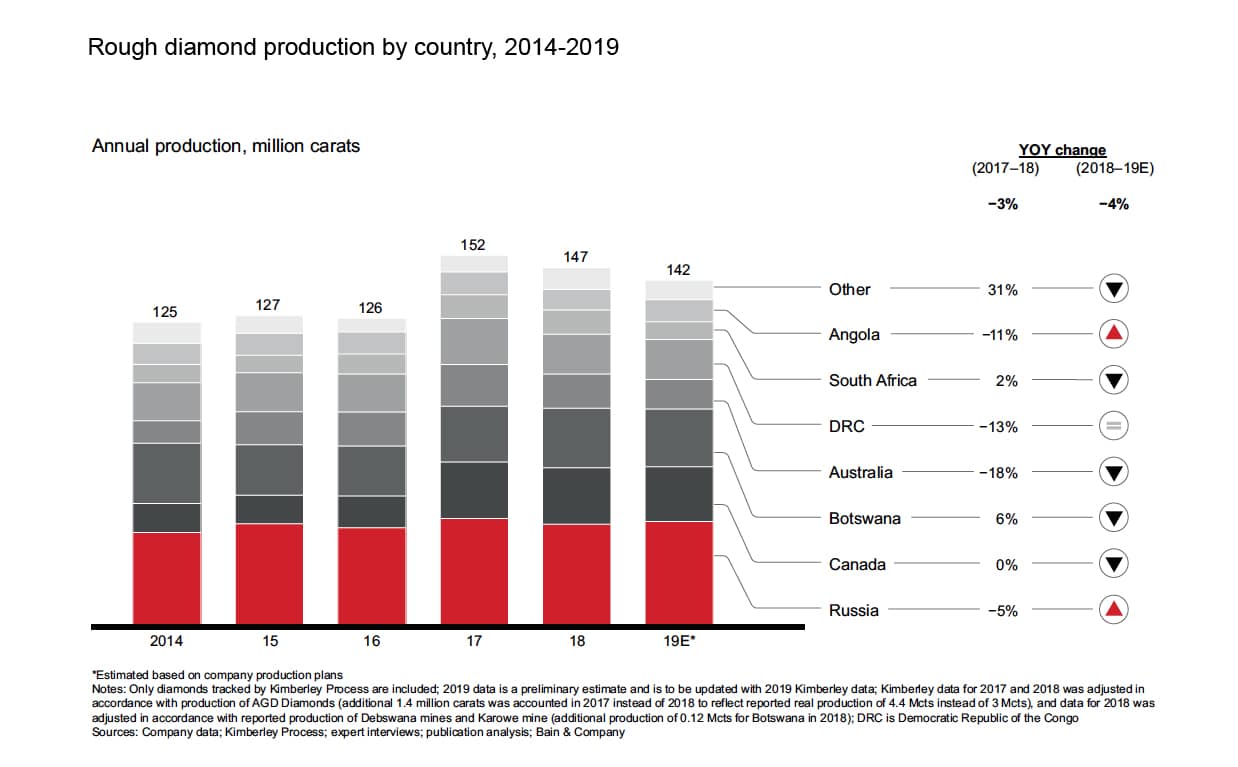

The challenges in the supply chain caused mining company revenues to fall by a substantial 25 percent, the report says, noting a ripple effect that was by near record-high rough diamond production in the beginning of 2019, which was followed by lower-than expected demand for polished diamonds, causing a ripple effect through the supply chain.

Rough diamond producers responded to midstream pressure by increasing their inventory levels and offering more flexible purchasing terms, as well as cutting rough diamond prices by 5 percent. Smaller mining companies lowered prices by 7 percent to 10 percent to minimize inventory.

Cutters and polishers reduced rough diamond purchases about 30 percent to off-load inventory and improve their cash flow.

Based on historic experience, the report notes, the market typically returns to pre-crisis levels within one to two years. “We expect the midstream to clear its inventory backlog in the beginning of 2020, bringing a better year for the industry. However, based on our historical analysis, the industry is not likely to fully recover in 2020 because of ongoing supply–demand inequality and limited growth of financing options for midstream players,” the report states.

“Major diamond producers have not announced substantial mining plan cuts, and we do not expect significant retail growth in 2020, as consumers brace for a global recession. The industry will have a stronger chance to rebalance and grow in 2021,” it continues.

FOUR KEY TRENDS SHAPING THE INDUSTRY

The AWDC/Bain report points to four key trends are currently shaping the diamond industry:

The rapid growth of e-commerce, which has a more efficient supply chain operations that require less inventory on hand. This, its states, will require a rethink the business model used by most midstream players.

Marketing spending in general is increasing, with the diamond jewelry industry is facing increased competition from the experiences and electronics categories.

The lab-grown diamond market, which grew 15 percent to 20 percent in 2019. Select jewelry designers and retailers are beginning to use lab-grown diamonds.

There is a heighted focus on sustainability and social welfare, with both consumers and the professional community seeking transparency throughout the pipeline to ensure diamonds are sourced responsibly and produced sustainably.