Home » Diamonds blog » SIGNIFICANT SHIFT TO ONLINE COMMERCE ASSISTS BRANDS GAIN LARGER SHARE OF FINE JEWELRY MARKET

Focus on

DIAMOND JEWELRY

SIGNIFICANT SHIFT TO ONLINE COMMERCE ASSISTS BRANDS GAIN LARGER SHARE OF FINE JEWELRY MARKET

In contrast to most other luxury products, the fine jewelry category is not dominated by major brand names, at least in terms of sales value. For although the public is a generally aware of names such as Tiffany, Cartier and Bulgari, in terms of actual transactions they currently account for only about 20 percent. But that is likely to change.

According to the recently released State of Fashion Watches & Jewelry report, prepared by the consulting House McKinsey & Company with the support of with Business of Fashion, by 2025 brands will hold between a 25 percent and 30 percent market share. This means that $80 billion to $100 billion up for grabs.

A key factor in the expansion of this sector jewelry market is the growing share of online sales. Simply stated, consumers are more inclined to make large ticket purchases without having handled the product if they are already familiar with the name of the vendor. In this department the brands have a clear advantage.

Indeed, according to data from Agility quoted in the McKinsey report, 60 percent of affluent consumers prefer to use a brand’s own website when making a high-ticket purchase. However, this does not rule out prominent multi-brand e-tailers like Net-a-Porter, although some may argue that it, too, has achieved a degree of brand recognition on its own.

DIRECT-TO-CONSUMER BRANDS

The most well-known jewelry houses have the currently have the advantage of name recognition, not to mention size, investment power and brand equity. But, says the McKinsey report, they will need to be agile and quick to stay ahead of other a number of other players who are expected enter the market.

Among the newcomers are what McKinsey refers to as direct-to-consumer (DTC) brands, which most often have a digital marketing first approach, and often a very specific value proposition, like sustainability. They could account for 20 percent of growth in the branded market by 2025, the report states.

Certain of these DTC jewelry brands saw growth in sales of literally hundred pf percent during the early months of the COVID crisis. One such company was Kendra Scott, which began started offering virtual try-ons, using augmented reality and machine learning technology

“More nimble by virtue of their often digital-first presence and close connection to consumers, these players will aggressively acquire customers through social media and paid marketing, testing and iterating on messages and techniques to most efficiently capture the target consumer,” the McKinsey report says.

A sample of a Kimberley Process Certificate issued by the European Union.

RECREATING THE ‘MAGIC’ THE BRAND EXPERIENCE

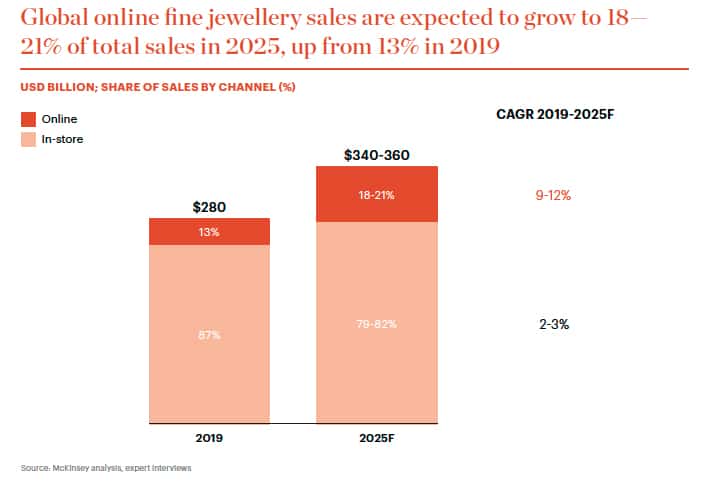

According to McKinsey, McKinsey’s analysis the ecommerce jewelry market will double in size between 2019 and 2025, attaining a market share 18 to 21 percent of global fine jewelry sales, or $60 to $80 billion in annual turnover.

But investing in the technology and know-how required to take advantage of the surge could be a double-edged sword, with even some of the larger players finding that they are becoming over-extended. In its 2020 annual report, the Danish fashion jewelry giant Pandora revealed that a higher share of online sales was impacting negatively on its profit margins.

The one challenge that the brands will have to contend with is reinvent the “magical” experience that is part and parcel of shopping in one of their stores.

How do create in a virtual setting the rush and feeling of wellbeing that the customer seeks out. After all, buying high-end jewelry online cannot be the same as purchasing toothpaste, or books, or even video games.

“To start,” McKinsey suggests in its report, “companies will need to define the role of each digital channel and clearly articulate the use cases, or needs, that the channel should address for both the consumer and the business. With clearly defined use cases, jewelers can then better determine what type of ‘magic’ is needed to deliver, or over-deliver, for the customer. Winners will master capturing the emotional dimension of the purchase and will elevate the experience beyond that of buying everyday items online.