Blog

Home » Diamonds blog » THE PROMISE AND COST OF MINING DIAMONDS IN FRIGID WEATHER CONDITIONS

Focus on

There are a range of variables that factor in the economics of the diamond business, some of which are likely to be the deciding factor whether a business is profitable or not. Elements like the quality of the diamond itself, the skill and proficiency of the cutters and polishers, market demand and the general state of the economy are all accepted as standard issues that will affect the profitability of the business. But there is one that many would not think about – the weather.

To be fair, we are not simply talking about regular weather pattern, but rather extremely cold temperatures, like the types that one would expect in the Arctic Circle. In the diamond industry, in particular the rough diamond mining sector, these are not out of the ordinary. The world’s two largest producers of rough diamonds are Russia and Canada, and almost all the mines in both countries are within 2,600 kilometers of the North Pole. These are areas where temperatures can fall below 50 degrees centigrade.

The temperature itself has no specific effect on the diamond itself, but it does fundamentally affect the way in which they are mined. Mining in frigid conditions is not only difficult but the wear and tear on equipment is substantial, and considerably greater volumes of energy are expended. In short, the cost per carat of diamond produced is considerably higher than it is in the hotter climates in which diamond mining traditionally has taken place, in Africa, South America and India.

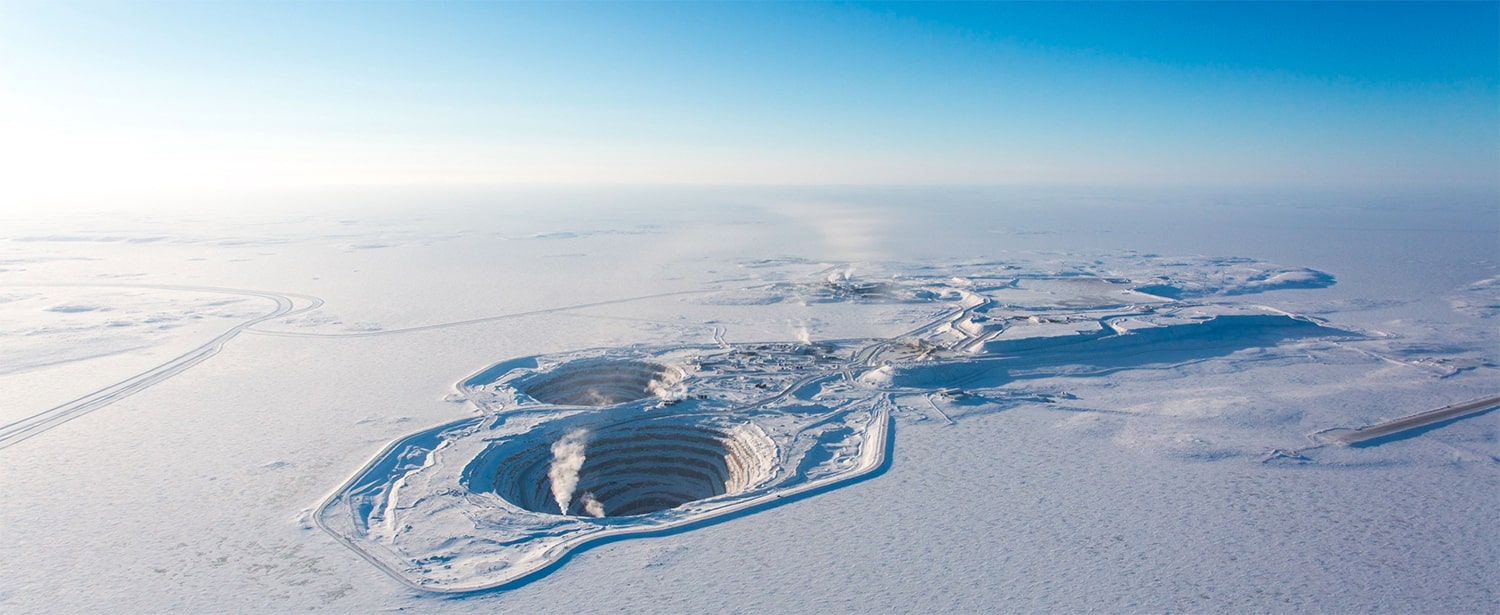

RUSSIA PIONEERS TO CONCEPT OF ARCTIC DIAMONDS

Prior to the discovery of the first diamond-rich kimberlite pipe at Zarnitsa in the Soviet autonomous Republic of Yakutia in 1957, kimberlite mining activity, which accounts for the bulk of rough diamonds produced, was concentrated exclusively in warmer regions Africa.

The first kimberlite pipe to be actively developed in the then-Soviet Union was at Mir and by 1959 it was producing industrial diamonds. Despite the challenges of working in the remote region, with winter temperatures down to minus 60 degrees, no roads, and extreme distances to industrial centers, the Soviets were undeterred. In 1961, they began developing the Aikhal pipe, located almost at the Arctic Circle. To supply energy to the plants and open-pit mines, they built the world’s first hydroelectric power station on permafrost.

The costs were enormous, and it is extremely unlikely that they would ever have been considered anywhere else other than the Soviet Russia, where national pride and Marxist economics generally trumped profit-and-loss business common sense. Much of this happened in secret, since the Soviet government considered their diamond resources to be strategic assets.

Russia’s Mir mine, which was built above the kimberlite pipe that because the first cold-weather deposit to be developed in 1959.

An Alrosa geologist working with ore samples in the frozen temperatures that are autonomous region of Yakutia.

Indeed, it is unlikely that the Canadian diamond industry, which is located mainly in the Northwest Territories at latitudes similar to the mines in Russia, would have ever come to be had it not been for the collapse of the Soviet Union in the early 1990s, and the export of expertise garnered by the Russians during the period that only they were mining in cold-weather climates.

CANADA FOLLOWS, BUT THEN THE GOING GETS ROUGH

In 1991 two geologists, Chuck Fipke and Stewart Blusson, found evidence of diamond-bearing kimberlite pipes about 200 miles north of the town of Yellowknife in the Northwest Territories. The first of these pipes was developed by BHP Billiton into the Ekati Diamond Mine, which produced Canada’s first commercial diamonds in 1998. Ekati is today owned by the Dominion Diamond Corporation.

The second was Diavik, located about 300 kilometers southeast of Yellowknife. A joint venture between a joint venture between the Rio Tinto Group, which hold 60 percent, and Dominion Diamond Corporation, it commenced production in 2003.

By 2006, three major mines were producing over 13 million carats of gem-quality diamonds per annum, positioning Canada as the third-largest producer of diamonds in the world.

But much of the excitement that gripped the Canadian diamond mining industry 20 years ago is no longer there, and to a large degree it is result of the cold weather climate. It’s not a question of whether there are sufficient diamond resources or not, but rather whether it is worth going to the expense of extracting them.

Every operating mine in Canada produces rough diamonds priced below the global average, with all but one mine producing diamonds worth more $100 per carat. De Beers’ African mines, in contrasts, and Alrosa’s Russian mines average more than $160 a carat. Some smaller mines, like Gem Diamonds, which is mining mainly in Lesotho, and Lucara Diamond Corp., which is mining in Botswana, both in warm climates, respectively had average selling prices of $2,131 and $502 per in 2018.

But the weather and the conditions it creates demand better than average per carat returns, and Canada is not delivering the goods. “You look at these diamond mines, you’ve got your own road, your own airstrip, your own power grids,” said Tom Hoefer, executive director of the NWT & Nunavut Chamber of Mines, speaking to the Bloomberg news service. “That may be okay if you’ve got a world class deposit, but not everybody is mining world class assets.”