Blog

Home » Diamonds blog » WHILE PRICES VARY DRAMATICALLY, RETAILERS STILL BLUR SEPARATION OF NATURAL AND LAB-GROWN DIAMOND MARKETS

Focus on

Photo: Uzunov Rostislav on Pexels.com.

One of the debates that raged throughout the diamond industry about a decade ago, when it became apparent that laboratory-grown stones were not a curiosity nor a passing phase, was the degree to which they would come to challenge demand for natural diamonds, or whether they would constitute a new category, essentially expanding the jewelry market in general.

Today, years after their presence in the market first became evident, it is still difficult to judge which of the two alternatives is more relevant, or whether it is even still premature to reach a definitive finding.

There is certainly some evidence of separation between natural and lab-grown diamonds, and a growing understanding in the market that, while consumers may still be inept in differentiating between them, their pricing structures are not interlinked, nor are the economics by which each operates.

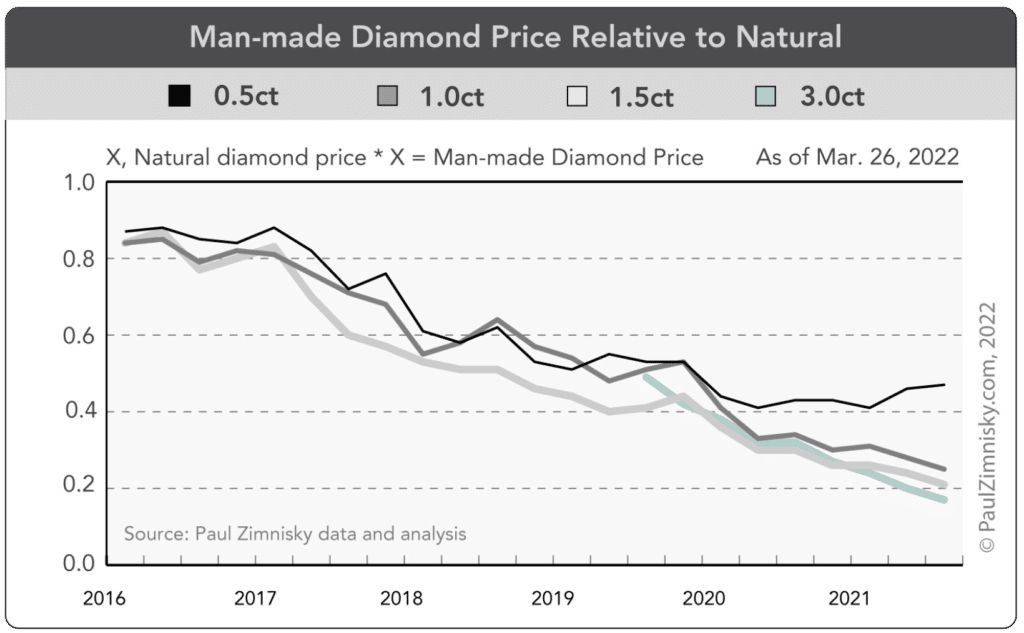

In the early days, the price of lab-grown stones was directly connected to the price of natural goods, and was articulated as a discount of the figure quoted for a natural stone of particular size and quality. That discount grew dramatically as the volume of lab-grown goods in the market mushroomed, and the average price per carat of LGD plummeted. It then became somewhat meaningless when De Beers launched its Lightbox jewelry line in 2018, with good-quality lab-grown stones being sold at fixed prices that were completely divorced from those being quoted in the natural diamond market.

What clearly was apparent was that the price of lab-grown goods were coming down, and fast. How far into the abyss they would go was anybody’s guess, with a real possibility being a repeat of that which occurred in the colored gemstone sector, where synthetics came to be sold a miniscule fraction of what was being paid for the natural product.

Source: Paul Zimmisky.com/Natural Diamond Council

CANNIBALIZATION OF THE NATURAL DIAMOND

It would appear that one of the reasons that consumers continue to group natural and lab-grown stones together is a because it is economically advantageous for jewelry retailers to perpetuate the perception that the two categories exist on single product continuum.

Writing in India’s Solitaire news outlet in late 2022, industry analyst Pranay Narvekar noted that lab-grown diamonds’ success in achieving significant retail store penetration in the United States over the past two to three year has been been achieved through cannibalization of the natural diamond jewellery market. To manage this, LGD jewelry was explicitly offered as a cheaper alternative to natural diamond jewellery.

“Retailers have pushed larger LGD product to consumers at the same price point for natural jewellery as their margins and profits are much higher in LGD jewellery,” Narvekar wrote. “The reduction in LGD wholesale prices in 2022 was not fully passed on to the retail consumers, and further padded retailer margins.”

“To date, the LGD market growth was during a period of secular market growth, and the pain on the natural pipeline had been masked,” he continued. “In 2022 Christmas season and in 2023, we will be facing a shrinking overall jewelry market along with increasing LGD penetration, and the full impact of the cannibalisation will now be felt on the natural pipeline.”

THE DOOMSDAY SCENARIO

But referencing Abraham Lincoln’s famous observation about the difficulty of fooling all of the people all of the time, the change in consumer attitudes is likely to occur when they realize that the costly piece of jewelry they bought several years ago is today worth only a very modest percentage of its original value.

“While retailers, driven by higher margins, have clearly picked their side, the result of this battle between LGD and natural diamonds could well be determined by actions and decisions taken by individual pawn shops across the U.S., as they set the buy-back prices for natural and LGD diamonds,” Naverkar said.

That doomsday scenario or moment of serendipity, depending on which side of the fence you sit, clearly has not yet happened. Over the past year the lab-grown diamond market’s share has almost doubled, and about 10 percent sold in the United States were grown synthetically in a factory.

Reporting in December, MVI Marketing a market research operation that is closely connected to the lab-grown diamond industry, reported that 46 percent of jewelry retailer respondents in its latest study said lab-grown diamonds are “absolutely” taking business away from their mined diamond business.

“This research study confirms that the lab-grown diamond disruption has gone far beyond the borders of the USA and is now seeing increasing consumer demand in markets across the globe,” said Liz Chatelain, President, and co-founder of THE MVEye, MVI’s consultancy business. “And there is certainly clear evidence that the mined diamond business is now being cannibalized.”

Some 87 percent of jewelry retailers polled said they are “satisfied” or “very satisfied” with their decision to sell lab-grown diamonds. Given the larger profit margins, such satisfaction should be self-evident.

But, noted the study, or those retailers who do not sell lab-grown diamonds, one of their two main reasons were: “The retail value could drop drastically, leaving me with angry customers.” The other main reason was “We believe in mined only.”